At two years old, my son was diagnosed with Acute

Lymphoblastic Leukemia. He is

twenty-seven years old now. Up until

very recently, when I tried to get insurance coverage for him, companies would

decline him based on his medical history.

Fortunately, one carrier, Anthem Blue Carrier offered him coverage.

Unfortunately, they increased their rate by an

additional 25% because he had leukemia twenty one years prior but he needed medical coverage and I was just glad that someone would

insure him and he paid those rates for the next few years until he switched

over to Kaiser.

He’s been with Kaiser for the last few years and initially,

the premiums were $160 per month and after six months, they increased to $209

and after six more months, it went up to $220.

In September , he received notification from Kaiser that they would be

discontinuing his current coverage because it didn't meet the ACA minimum

standards but not to fret, they would automatically insure him under a new plan.

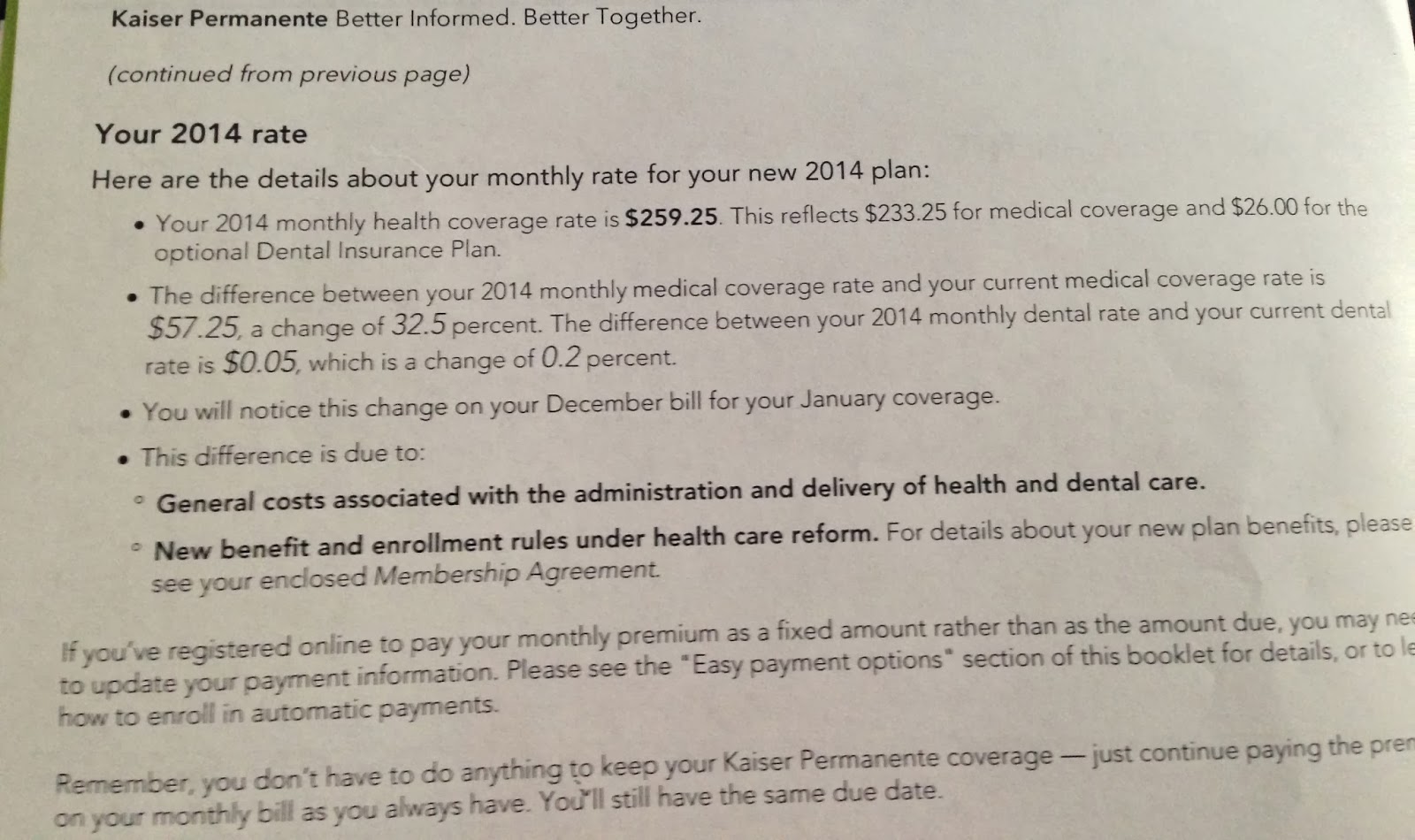

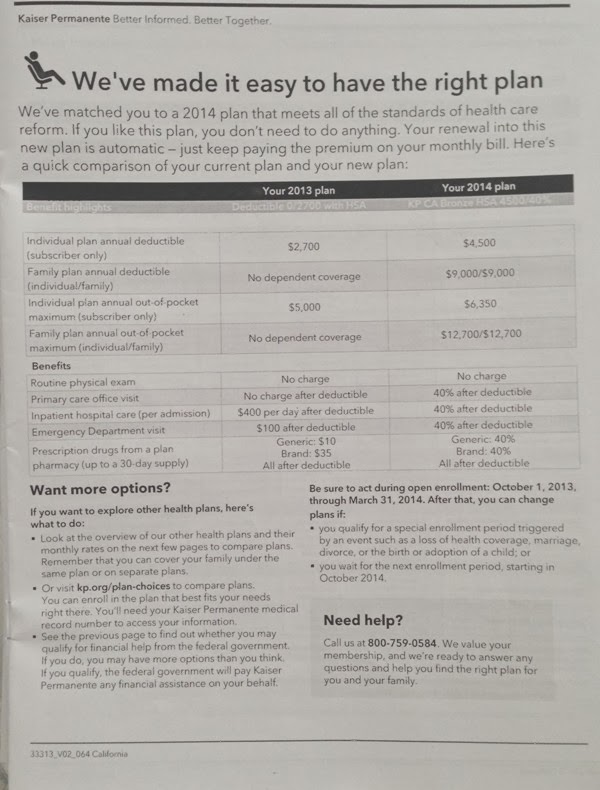

As you’ll notice , his rate would increase by 32.5% under their proposed plan and

although the increase is not significant, the coverage between his current plan

and the plan they were proposing were not similar . The $1,800 jump in deductible alone is ridiculous. Basically, they wanted to

provide less coverage for more money.

I decided to check out the California Insurance Exchange

website to see what my son's options were. Not

only did I sign him up for better coverage with Kaiser but it's also at a lower price because he will receive $91 in premium assistance.

I guess my point is, don’t listen to half of what you hear

from people. Demand proof of what they are telling you and if they can't offer proof, then their sole intention is to fan the flames of mass hysteria. Honestly, if you need to wag the finger of blame, wag it at the insurance companies.

There there, now. It wasn't so scary after all, was it?

No comments:

Post a Comment